All Categories

Featured

Table of Contents

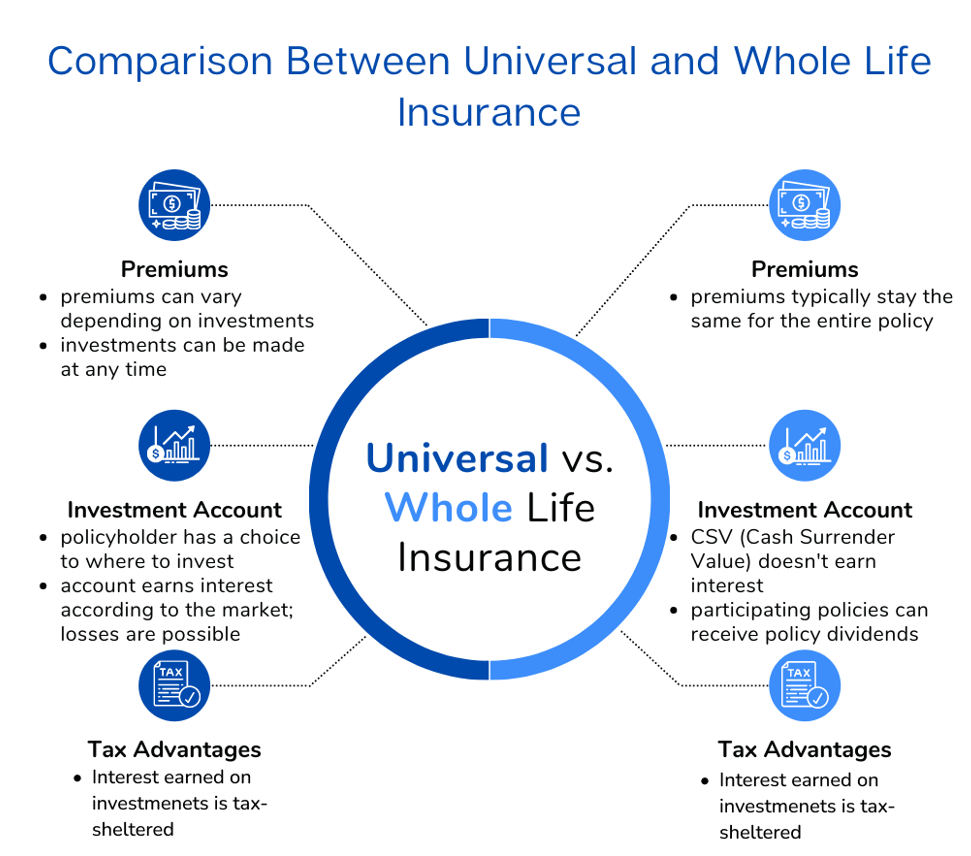

The are whole life insurance policy and universal life insurance coverage. The money worth is not added to the fatality advantage.

After one decade, the cash money worth has actually expanded to around $150,000. He takes out a tax-free funding of $50,000 to start a business with his sibling. The plan funding rates of interest is 6%. He settles the financing over the next 5 years. Going this course, the rate of interest he pays returns right into his plan's money worth rather than a banks.

Non Direct Recognition Life Insurance Companies

Nash was a finance professional and follower of the Austrian institution of economics, which advocates that the worth of items aren't explicitly the result of standard financial frameworks like supply and demand. Rather, individuals value cash and products differently based on their financial status and requirements.

Among the mistakes of standard banking, according to Nash, was high-interest rates on loans. Too numerous people, himself consisted of, obtained into monetary trouble because of reliance on financial organizations. So long as financial institutions established the rates of interest and lending terms, individuals didn't have control over their own wealth. Becoming your very own banker, Nash determined, would certainly place you in control over your financial future.

Infinite Banking requires you to have your financial future. For goal-oriented individuals, it can be the ideal financial device ever. Right here are the advantages of Infinite Banking: Arguably the single most advantageous element of Infinite Banking is that it boosts your capital. You don't require to undergo the hoops of a traditional bank to obtain a funding; simply request a policy lending from your life insurance policy business and funds will be provided to you.

Dividend-paying whole life insurance policy is extremely reduced threat and offers you, the insurance holder, a wonderful offer of control. The control that Infinite Financial uses can best be grouped into two groups: tax obligation advantages and possession securities.

Be My Own Bank

When you use entire life insurance for Infinite Financial, you get in into an exclusive contract in between you and your insurance coverage firm. These securities might differ from state to state, they can consist of protection from asset searches and seizures, protection from reasonings and protection from financial institutions.

Entire life insurance coverage plans are non-correlated possessions. This is why they work so well as the financial structure of Infinite Financial. Regardless of what takes place in the market (supply, actual estate, or otherwise), your insurance policy maintains its worth.

Market-based financial investments expand riches much faster but are revealed to market variations, making them inherently high-risk. What happens if there were a third bucket that provided security yet additionally modest, guaranteed returns? Entire life insurance is that 3rd container. Not only is the rate of return on your entire life insurance policy policy ensured, your survivor benefit and costs are additionally guaranteed.

This framework aligns perfectly with the principles of the Continuous Riches Method. Infinite Banking attract those seeking higher economic control. Here are its major advantages: Liquidity and availability: Plan finances offer prompt accessibility to funds without the constraints of standard small business loan. Tax performance: The cash worth expands tax-deferred, and plan finances are tax-free, making it a tax-efficient device for developing riches.

Unlimited Life Policy

Asset defense: In several states, the cash value of life insurance coverage is safeguarded from lenders, including an extra layer of economic security. While Infinite Banking has its qualities, it isn't a one-size-fits-all solution, and it comes with significant drawbacks. Right here's why it might not be the very best strategy: Infinite Financial frequently needs detailed policy structuring, which can perplex insurance holders.

Envision never ever having to worry about bank lendings or high passion rates again. That's the power of limitless financial life insurance.

There's no set lending term, and you have the freedom to choose the repayment schedule, which can be as leisurely as settling the lending at the time of fatality. This flexibility prolongs to the maintenance of the car loans, where you can select interest-only payments, keeping the financing balance level and workable.

Holding money in an IUL repaired account being credited passion can commonly be better than holding the cash money on down payment at a bank.: You've always fantasized of opening your very own bakery. You can borrow from your IUL plan to cover the initial costs of renting out a room, purchasing tools, and employing personnel.

Infinite Banking Video

Personal finances can be acquired from typical banks and credit rating unions. Borrowing cash on a credit score card is generally really expensive with annual portion rates of passion (APR) frequently reaching 20% to 30% or more a year.

The tax therapy of plan loans can differ dramatically depending on your country of home and the particular terms of your IUL policy. In some regions, such as North America, the United Arab Emirates, and Saudi Arabia, policy car loans are generally tax-free, offering a considerable advantage. In other territories, there might be tax ramifications to think about, such as prospective tax obligations on the finance.

Term life insurance just provides a survivor benefit, without any type of cash money worth build-up. This means there's no cash money worth to obtain versus. This write-up is authored by Carlton Crabbe, Ceo of Funding forever, a professional in giving indexed universal life insurance policy accounts. The information offered in this article is for instructional and informative objectives just and ought to not be understood as monetary or financial investment advice.

Nonetheless, for lending police officers, the comprehensive regulations enforced by the CFPB can be seen as difficult and limiting. First, financing police officers usually say that the CFPB's guidelines develop unnecessary red tape, bring about more documentation and slower car loan handling. Regulations like the TILA-RESPA Integrated Disclosure (TRID) policy and the Ability-to-Repay (ATR) needs, while focused on safeguarding customers, can result in delays in closing deals and boosted operational prices.

{kind=link}

Latest Posts

Whole Life Banking

Be Your Own Bank: 3 Secrets Every Saver Needs

Non Direct Recognition Whole Life Insurance